")

Retail meaning is integral to both consumer behavior and business strategies. What is retail? At its core, retail involves the direct sale of goods or services to consumers for personal use. This definition of retail spans a wide array of business types, ranging from charming local stores to expansive multinational chains. Understanding the meaning of retail is essential for those seeking to make informed purchasing decisions, as well as for businesses aiming to thrive in a market where competition is fierce. Retail, often considered the final step in the supply chain, ensures that products reach the public through a variety of channels, including traditional brick-and-mortar stores, online platforms, and mobile applications. This guide is designed to provide comprehensive insights into what retail is in 2024, catering to both seasoned retailers and newcomers eager to grasp the evolving definition of retail and its influence in the market.

What is Retail?

Retail refers to the process of selling goods or services directly to consumers. It involves a wide range of activities, including product sourcing, inventory management, pricing, marketing, and customer service. Retailers serve as intermediaries between manufacturers or wholesalers and end consumers, ensuring that products reach the right customers at the right time. The retail industry acts as a bridge between producers and consumers, connecting the supply and demand sides of the market.

What is Retail Industry?

The retail industry, a vital and constantly evolving sector, significantly contributes to the economy and the consumer market. This detailed guide aims to elucidate the meaning of retail, offering a comprehensive exploration of the retail industry. It delves into the industry's definition and its critical role, elucidating how the retail sector operates. The guide further categorizes various types of retail businesses and retail store formats, while also examining the fundamental functions of a retail business. Highlighting the world's leading retailers, this guide serves as an essential resource for anyone interested in understanding what retail is and its implications. It is designed to benefit aspiring entrepreneurs, marketing professionals, and those intrigued by the complexities and dynamics of the retail landscape, ensuring a deep understanding of the retail industry's meaning and significance.

Importance of the Retail Industry:

The retail industry holds significant importance in driving economic growth and creating employment opportunities. It contributes to GDP growth, stimulates consumer spending, and fosters competition and innovation. Retail businesses create jobs across various sectors, including sales, marketing, logistics, and customer support. Moreover, retail establishments often serve as community hubs, shaping local economies and enhancing social interactions.

How Retail Works?

Retail operates through a series of interconnected processes and functions. Let's explore how retail works:

- Product Sourcing: Retailers source products from manufacturers, wholesalers, or distributors. They consider factors such as product quality, price, availability, and alignment with customer preferences and market trends.

- Inventory Management: Retailers manage inventory to ensure product availability and avoid stockouts or overstocking. This involves monitoring stock levels, forecasting demand, and optimizing reorder points to maintain a balanced inventory.

- Pricing Strategies: Retailers develop pricing strategies based on factors such as production costs, market competition, customer demand, and perceived value. Pricing decisions aim to strike a balance between profitability and attracting customers.

- Marketing and Promotion: Retailers employ various marketing techniques to reach their target audience and promote their products or services. This includes advertising, digital marketing, social media campaigns, and in-store promotions to create awareness and drive customer engagement.

- Store Operations: For physical retailers, store operations are crucial. This includes managing store layouts, visual merchandising, creating an inviting ambiance, and ensuring a seamless shopping experience for customers.

- E-commerce and Omnichannel Strategies: With the rise of e-commerce, retailers often adopt omnichannel strategies to cater to changing consumer preferences. This involves integrating online platforms, mobile apps, and physical stores to provide a seamless shopping experience across channels.

- Customer Service: Retailers prioritize excellent customer service to build customer loyalty and enhance the overall shopping experience. This includes providing knowledgeable staff, handling inquiries and complaints promptly, and offering personalized assistance.

- Sales and Checkout: The sales process involves assisting customers, answering questions, and guiding them through the purchase journey. Retailers utilize point-of-sale systems to process transactions efficiently and securely.

- Post-Sale Support: After the sale, retailers may offer services such as returns and exchanges, warranty support, and customer feedback mechanisms to ensure customer satisfaction and retention.

Also Read: Future of Retail industry in India

Types of Retail Businesses

Retail businesses can be categorized based on their operational models and how they reach their customers. Here are some common types of retail businesses:

1. Brick-and-Mortar Retailers

Brick-and-mortar retailers operate physical stores where customers can browse and purchase products in person. These businesses range from small local shops to large national chains. They emphasize customer service and the tactile experience of shopping.

2. E-commerce Retailers

E-commerce retailers sell products online through their websites or online marketplaces. These businesses leverage technology to reach a global audience, offering convenience and often a wider selection than physical stores. E-commerce retailers focus on efficient logistics and user-friendly online experiences.

3. Direct Selling

Direct selling involves businesses selling products directly to consumers, often through personal presentations, home parties, or online platforms. This model includes companies that use independent sales representatives to market and sell their products, such as cosmetics or home goods.

4. Franchise Retailers

Franchise retailers operate under a franchising agreement, where a franchisee pays for the right to use the brand, business model, and support of an established company. This model allows for rapid expansion and brand recognition, as seen with fast-food chains and convenience stores.

5. Multichannel Retailers

Multichannel retailers combine both physical stores and online platforms to reach customers through multiple touchpoints. This approach allows businesses to offer a seamless shopping experience, integrating in-store, online, and mobile sales channels.

6. Direct-to-Consumer (DTC)

Direct-to-consumer businesses bypass traditional retail channels, selling products directly to customers through their own branded websites or pop-up shops. This model allows for greater control over the customer experience and often involves subscription services or personalized products.

7. Catalog Retailers

Catalog retailers sell products through printed or digital catalogs, allowing customers to place orders via mail, phone, or online. This model provides convenience for consumers who prefer browsing a curated selection of products from home.

8. Mobile Retailers

Mobile retailers operate out of mobile units, such as food trucks or traveling boutiques. These businesses bring products directly to customers at various locations, events, or markets, offering flexibility and unique shopping experiences.

9. Subscription Retailers

Subscription retailers offer products or services on a recurring basis, such as monthly boxes of curated items, meal kits, or digital content. This model provides a steady revenue stream and builds long-term customer relationships through convenience and personalized offerings.

Types of Retail Stores

Retail stores are physical locations where goods are sold directly to consumers. These stores vary widely in terms of their size, product offerings, and target markets. Here are some common types of retail stores:

1. Department Stores

Department stores are large establishments divided into various sections, each offering a specific type of product. They typically carry a wide range of items, including clothing, home goods, electronics, and beauty products. Department stores are known for their broad selection and often provide a more upscale shopping experience.

2. Specialty Stores

Specialty stores focus on a specific category of products. These stores offer deep assortments in their chosen niche, such as bookstores, toy stores, and sports equipment shops. Specialty stores often provide expert knowledge and personalized customer service.

3. Supermarkets

Supermarkets are large, self-service grocery stores that offer a wide variety of food and household products. They are designed to meet the everyday needs of consumers, featuring sections for fresh produce, dairy, meats, and non-perishable items. Supermarkets emphasize convenience and competitive pricing.

4. Convenience Stores

Convenience stores are small retail outlets that offer a limited range of everyday items, such as snacks, beverages, and basic groceries. They are typically located in easily accessible locations and are open for extended hours, catering to quick and last-minute purchases.

5. Discount Stores

Discount stores offer a broad range of products at lower prices than traditional retail outlets. They often achieve these lower prices through bulk purchasing and efficient distribution. Examples include dollar stores and warehouse clubs, which focus on providing value and savings.

6. Pop-Up Shops

Pop-up shops are temporary retail spaces that appear for a short duration in various locations. They are often used to create buzz around new products, test market demand, or take advantage of seasonal sales opportunities. Pop-up shops offer a unique shopping experience and can attract attention quickly.

7. Warehouse Clubs

Warehouse clubs are membership-based stores that sell products in bulk at discounted prices. These stores cater to both individuals and businesses looking to purchase large quantities of goods. Membership fees are typically required to shop at warehouse clubs, which offer access to exclusive deals.

8. Category Killers

Category killers are large specialty stores that dominate a particular product category, offering an extensive range of items within that category. These stores, such as home improvement giants or electronics superstores, often provide competitive pricing and vast selections, making it difficult for smaller competitors to thrive.

9. Hypermarkets

Hypermarkets combine the features of supermarkets and department stores, offering a wide range of food and non-food items under one roof. These large retail spaces are designed to provide a comprehensive shopping experience, with sections for groceries, clothing, electronics, and household goods.

Retailer vs. Retailing

When diving into the world of retail, it’s essential to distinguish between the terms "retailer" and "retailing." While they might sound similar, they play different roles in the industry. Let’s break it down in an engaging way that makes sense for entrepreneurs, businesspeople, and retailers alike.

What is a Retailer?

Think of a retailer as the friendly shopkeeper on the corner of your street or the massive department store downtown. A retailer is any business or individual that sells goods and services directly to you, the consumer. They are the last stop in the supply chain, where products go from the hands of manufacturers or wholesalers to your shopping cart.

Retailers come in many shapes and sizes. You’ve got your:

- Department Stores like Macy’s or Sears, offer a broad range of products under one roof.

- Specialty stores, such as GameStop or Foot Locker, focus on specific product categories.

- Supermarkets like Kroger or Tesco, provide a wide variety of food and household items.

- Convenience Stores such as 7-Eleven, perfect for those quick, last-minute purchases.

- Discount Stores like Dollar Tree, where you can find budget-friendly options.

- Each of these retailers offers something unique, whether it’s the convenience of a local store or the vast selection of a big department store. They interact with customers directly, manage inventory, and provide services that enhance the shopping experience.

What is Retailing?

Now, let’s shift gears to retailing. If a retailer is the actor on stage, retailing is the entire production, including backstage operations, marketing, and the grand performance. Retailing covers all activities involved in selling goods and services to consumers for their personal use. It’s the art and science behind the scenes that make your shopping experience possible.

Retailing encompasses:

- Marketing and Promotions: Crafting advertising campaigns, running sales promotions, and launching loyalty programs to attract and retain customers.

- Merchandising: Deciding what products to stock, how to price them, and how to display them to maximize sales.

- Customer Service: Ensuring that customers have a positive experience, from answering questions to handling returns.

- Sales Channels: Utilizing various platforms like physical stores, online shops, mobile apps, and social media to reach consumers.

- Logistics and Supply Chain Management: Coordinating the flow of goods from suppliers to store shelves or directly to customers’ doorsteps.

Retailing is the broader picture that includes every step taken to get a product from the manufacturer to the consumer. It’s all about creating a seamless and enjoyable shopping experience, whether it’s through a traditional store or an online platform.

Why It Matters

Understanding the difference between a retailer and retailing helps in recognizing the distinct roles they play. Retailers are the entities you interact with when you make a purchase. Retailing, on the other hand, involves the comprehensive processes and strategies that ensure those products are available and appealing to you.

For entrepreneurs and businesspeople, this distinction is crucial. It helps in making informed decisions about how to position their business in the market, optimize operations, and ultimately, delight their customers.

Retail Supply Chain

The retail supply chain consists of four key players, each playing a vital role in ensuring products are delivered efficiently from production to the consumer. Here’s a detailed look at each player and their responsibilities:

1. Manufacturers

Manufacturers are the creators of products. They take raw materials and transform them into finished goods ready for sale. Manufacturers are responsible for ensuring the quality and quantity of products meet market demands. They continuously innovate and improve products based on consumer feedback and market research.

2. Wholesalers/Distributors

Wholesalers or distributors act as intermediaries between manufacturers and retailers. They buy products in bulk from manufacturers and store them in large warehouses. By purchasing in large quantities, wholesalers can negotiate better prices. They then break down these bulk shipments into smaller quantities that are more suitable for retail stores. This step helps in managing inventory and ensures that products are available for retailers when needed.

3. Retailers

Retailers are the businesses that sell goods directly to consumers. They are the final link in the supply chain, making products accessible to the end-users. Retailers operate through various channels, including physical stores, online platforms, or a combination of both. They interact directly with consumers, providing customer service, handling returns, and creating an enjoyable shopping experience. Retailers manage their stock levels to ensure that they can meet consumer demand without overstocking or understocking.

4. Consumers

Consumers are the end-users who purchase and use the products. They are the driving force behind the entire supply chain. Consumer preferences and demands determine what products are produced, distributed, and sold. Their feedback is crucial for retailers and manufacturers to make improvements and innovations. Consumers influence market trends through their purchasing behavior and reviews.

How It Works

- Manufacturers: Produce goods and ensure quality.

- Wholesalers: Buy in bulk, store, and distribute to retailers.

- Retailers: Sell products to consumers through various channels.

- Consumers: Purchase and use the products, providing feedback.

Example Flow

- Step 1: A manufacturer produces electronics and ships them to a wholesaler.

- Step 2: The wholesaler buys these electronics in large quantities, stores them in a warehouse, and then distributes them in smaller quantities to different retailers.

- Step 3: Retailers, such as electronics stores or online shops, purchase these electronics from the wholesaler and offer them to consumers.

- Step 4: Consumers visit the retail stores or shop online to buy the electronics, using and reviewing them, which influences future manufacturing and retailing decisions.

Importance of Coordination

Efficient coordination among all players in the retail supply chain is crucial. It helps reduce costs, minimize delays, and improve customer satisfaction. Technologies like supply chain management software, real-time inventory tracking, and data analytics streamline these processes, ensuring products are available where and when consumers need them.

By understanding the roles and interactions of each player in the retail supply chain, businesses can manage their operations better, respond to market changes, and meet customer needs more effectively.

Retail Business Functions:

The success of a retail business relies on various functions and operations working harmoniously. Understanding these functions can help businesses optimize their operations and provide exceptional customer experiences. Here are some key retail business functions:

- Merchandising: The process of selecting, presenting, and promoting products to maximize sales and meet customer demand.

- Inventory Management: Efficiently managing inventory levels, ensuring product availability, minimizing stockouts, and optimizing turnover ratios.

- Pricing Strategies: Establishing competitive pricing structures that align with market dynamics, customer expectations, and business objectives.

- Customer Service: Providing exceptional customer experiences through knowledgeable and friendly staff, addressing inquiries, handling complaints, and fostering customer loyalty.

Also Read: How to increase footfall in retail store

Top Retailers Around the World:

The retail industry boasts numerous successful and influential retailers worldwide. Studying these retailers can provide valuable insights into their strategies and best practices. Here are some notable retailers around the world:

- Amazon: The global e-commerce giant known for its vast product selection, personalized recommendations, and expedited delivery services.

- Walmart: One of the world's largest retailers, offering a wide range of products at competitive prices through its extensive network of physical stores and e-commerce operations.

- Alibaba: A leading Chinese e-commerce conglomerate that operates various online marketplaces, facilitating B2B, B2C, and C2C transactions.

- Zara: A renowned fashion retailer known for its fast-fashion model, providing trendy and affordable clothing options through its global network of stores and online channels.

Final Words:

In conclusion, grasping the retail meaning and intricacies of the retail industry is crucial for individuals engaged or intrigued by this dynamic sector. This guide has provided a comprehensive overview, delving into its definition, significance, operational mechanisms, various business types, functions, global retail leaders, and additional learning resources. With this knowledge in hand, you can confidently navigate the retail landscape, seize its abundant opportunities, and make informed decisions to thrive in this constantly evolving industry.

FAQs on the Retail

1. What is retail, and how does it differ from wholesale?

Retail involves selling goods and services directly to consumers for their personal use. Retailers operate through physical stores, online platforms, or both. In contrast, wholesale refers to selling goods in large quantities to businesses or retailers, who then resell them to consumers. While wholesalers focus on bulk transactions and supply chain management, retailers prioritize customer interaction and providing a shopping experience.

2. What are the different types of retail businesses?

There are various types of retail businesses, each catering to different market needs. Key types include:

- Department Stores: Large stores offering a wide range of products across multiple categories.

- Specialty Stores: Focus on specific product categories, such as electronics or clothing.

- Supermarkets: Large self-service stores offering food and household items.

- Convenience Stores: Small stores with extended hours, offering everyday items.

- Discount Stores: Sell products at lower prices, often through bulk purchasing and efficient distribution.

- Online Retailers: Operate through e-commerce platforms, providing a broad selection of goods.

3. How important is customer service in retail?

Customer service is crucial in retail, as it directly affects customer satisfaction and loyalty. Excellent customer service helps build trust and positive relationships with consumers, leading to repeat business and positive word-of-mouth. Retailers must provide helpful, friendly, and efficient service to address customer needs, handle returns, and resolve issues promptly.

4. What role does technology play in modern retail?

Technology plays a significant role in modern retail by enhancing the shopping experience, improving operational efficiency, and facilitating better inventory management. Key technologies include:

- E-commerce Platforms: Enable online shopping and broaden the reach of retailers.

- Point of Sale (POS) Systems: Streamline transactions and track sales data.

- Customer Relationship Management (CRM) Software: Helps manage customer interactions and improve service.

- Inventory Management Systems: Ensure accurate stock levels and reduce overstocking or stockouts.

- Data Analytics: Provides insights into consumer behavior and helps in making informed business decisions.

5. How can retailers stay competitive in a changing market?

Retailers can stay competitive by adopting several strategies:

- Adapting to Market Trends: Stay updated with consumer preferences and market shifts to stock relevant products.

- Enhancing the Customer Experience: Offer personalized services, loyalty programs, and a seamless shopping experience across all channels.

- Leveraging Technology: Utilize modern technologies to streamline operations and improve customer interactions.

- Effective Marketing: Use targeted marketing campaigns to reach potential customers and retain existing ones.

- Efficient Supply Chain Management: Ensure a smooth flow of goods from suppliers to stores to meet consumer demand promptly.

Healthy, radiant skin has become a key part of everyday skincare routines, prompting consumers to look beyond cleansers and body washes to products that offer additional skincare benefits. Skin brightening soaps have gained popularity for their ability to cleanse while helping improve skin tone, reduce dullness, and maintain the skin's natural glow. Enriched with botanical extracts, vitamins, essential oils, and nourishing ingredients, these soaps are designed to support healthier-looking skin without compromising on hydration.

Rise in skincare-infused beauty products

With a growing preference for ingredient-led beauty products, consumers are increasingly choosing soaps formulated with turmeric, saffron, goat milk, vitamin C, aloe vera, and natural oils. While no soap can permanently change one's natural skin color, many can help remove impurities, improve skin texture, and enhance the skin's natural radiance with regular use. Here are five skin brightening soaps in India that stand out for their formulations and customer popularity.

Top 5 Skin Brightening Soaps in India for Naturally Radiant Skin

The Indus Valley Skin Brightening Mild Body Soap

If you're looking for one of the best skin brightening soaps for naturally glowing skin, The Indus Valley Skin Brightening Mild Body Soap is a great choice. Made with 100 percent organic and handmade ingredients, this gentle soap helps remove tan, cleanse impurities, and enhance the skin's natural radiance without stripping away moisture. Enriched with Mashobra Wild Honey, Papaya Fruit Extract, Olive Oil, Cold-Pressed Coconut Oil, and Mango Seed Butter, it deeply nourishes and hydrates the skin while supporting its natural moisture barrier. Crafted using the traditional cold-process method with a skin-friendly pH, it is suitable for all skin types, including sensitive skin. Free from SLS, parabens, artificial fragrances, and harsh chemicals, this soap leaves your skin soft, smooth, and visibly brighter with regular use.

2. Kozicare Skin Whitening Soap

Kozicare Skin Whitening Soap is formulated with ingredients such as glutathione, kojic acid, vitamin C, and moisturizing agents that aim to improve skin clarity and reduce the appearance of uneven skin tone. Regular cleansing helps remove impurities while supporting brighter-looking skin. The soap is widely used by consumers looking for a skincare routine focused on pigmentation concerns and dullness. Its creamy lather cleanses without leaving the skin feeling excessively dry, making it suitable for everyday use. Consistent use alongside sunscreen and a balanced skincare routine may help enhance the skin's natural radiance.

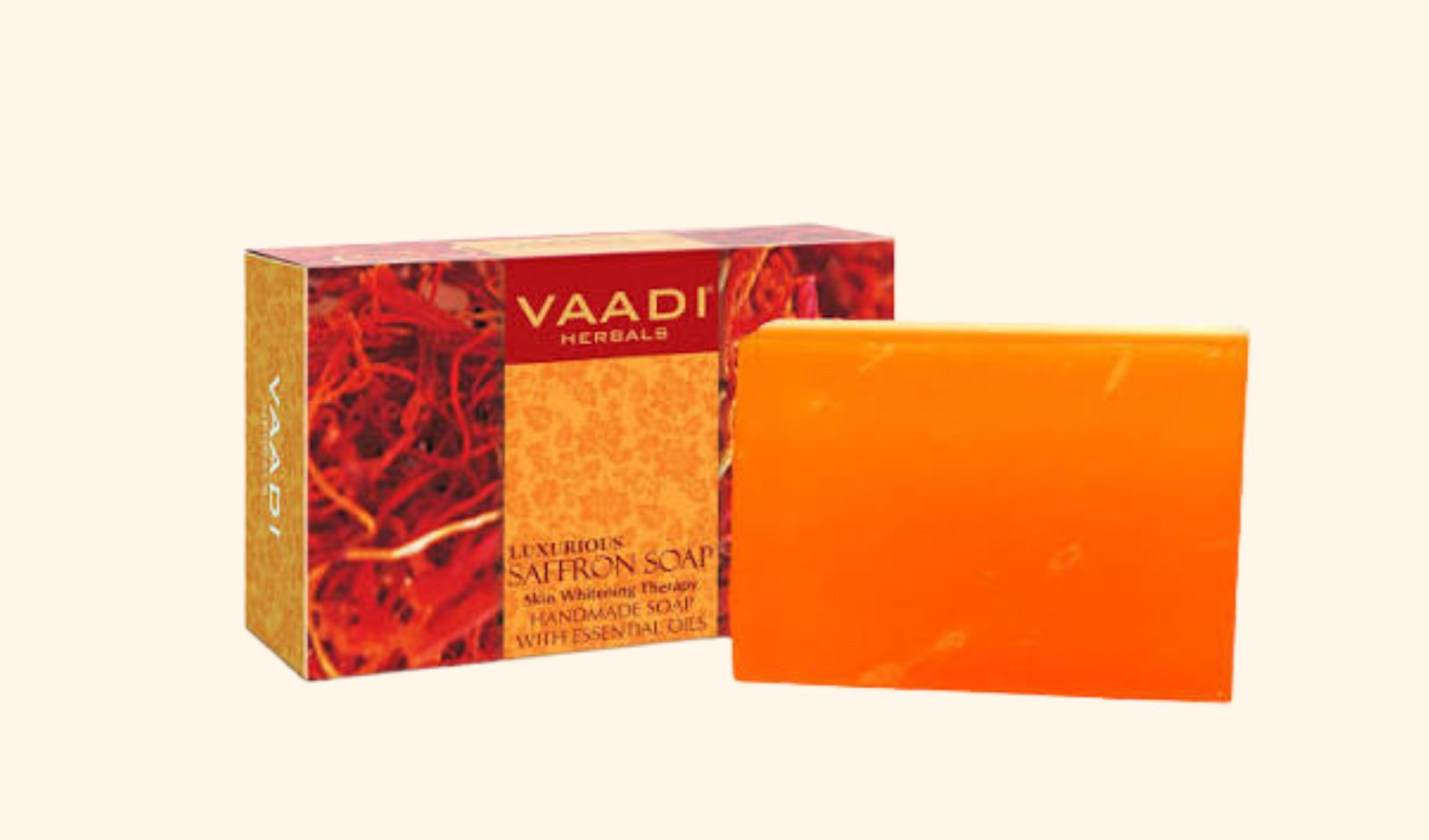

3. Vaadi Herbals Luxurious Saffron Skin Whitening Soap

Vaadi Herbals combines saffron, goat milk, and herbal extracts in this brightening soap designed to nourish and refresh the skin. Saffron has long been associated with improving skin luminosity, while goat milk provides gentle exfoliation through naturally occurring lactic acid. The soap helps cleanse deeply while leaving the skin soft and moisturized. Its herbal formulation appeals to consumers looking for affordable skincare products with traditional ingredients. Suitable for daily use, the soap works well for people seeking a brighter, smoother complexion without using harsh cleansing agents.

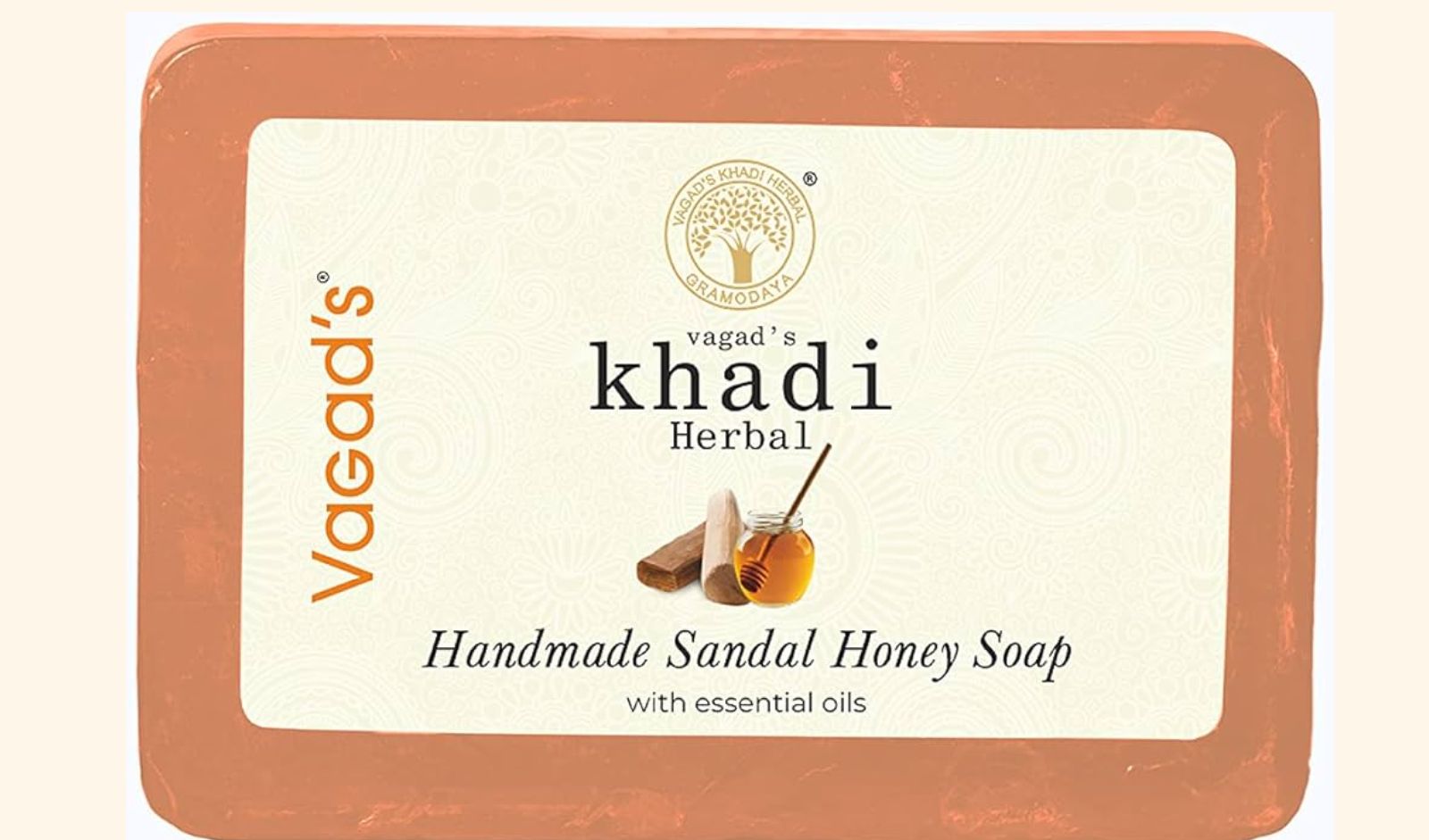

4. Khadi Natural Sandalwood & Honey Herbal Soap

Khadi Natural Sandalwood & Honey Herbal Soap offers a blend of sandalwood, honey, vegetable oils, and herbal ingredients that cleanse while nourishing the skin. Sandalwood is known for its soothing properties and ability to improve the skin's appearance, whereas honey acts as a natural humectant that helps retain moisture. The soap produces a rich lather that effectively removes dirt and excess oil without stripping away natural hydration. It is suitable for dry as well as normal skin types and is often preferred by consumers looking for Ayurvedic-inspired skincare products with gentle formulations.

5. Himalaya Herbals Neem & Turmeric Soap

Although primarily recognized for cleansing and maintaining healthy skin, Himalaya Herbals Neem & Turmeric Soap also contributes to a brighter-looking complexion by keeping the skin clean and reducing impurities that can make it appear dull. Neem offers antibacterial benefits, while turmeric is known for its antioxidant and skin-enhancing properties. Together, they help maintain clear, refreshed skin suitable for daily use. The soap is particularly beneficial for oily and acne-prone skin while providing gentle cleansing for regular skincare routines. Its trusted herbal formulation has made it a popular choice among Indian households.

Market Insights

India's skincare market continues to witness strong growth, driven by rising consumer awareness, increasing disposable incomes, and a greater focus on personal grooming. Demand for herbal, Ayurvedic, and clean-label skincare products has accelerated as consumers seek ingredient transparency and chemical-free alternatives. Skin brightening products remain one of the fastest-growing categories, with buyers increasingly preferring formulations enriched with vitamin C, turmeric, saffron, niacinamide, and plant-based extracts. The rapid expansion of e-commerce platforms and beauty-focused marketplaces has further improved accessibility, allowing both established and emerging skincare brands to reach consumers across urban and tier-II and tier-III cities.

Conclusion

Choosing the right skin brightening soap depends on individual skin type, ingredient preferences, and skincare goals. While these soaps cannot alter a person's natural complexion, they can help remove dirt, excess oil, dead skin cells, and environmental impurities that contribute to dull-looking skin. Products enriched with botanical extracts, moisturizing ingredients, and vitamins can support healthier, smoother, and more radiant skin when used consistently as part of a balanced skincare routine. Pairing these soaps with sunscreen, hydration, and a healthy lifestyle can further enhance the skin's natural glow and overall appearance.

Frequently Asked Questions (FAQs)

1. Do skin brightening soaps permanently lighten skin?

No. Skin brightening soaps do not permanently change your natural skin color. They help remove impurities, improve skin texture, and restore the skin's natural radiance.

2. Can I use a skin brightening soap every day?

Yes. Most skin brightening soaps are formulated for daily use. However, individuals with sensitive skin should perform a patch test before regular use.

3. Which ingredients are best for naturally radiant skin?

Ingredients such as turmeric, saffron, vitamin C, goat milk, aloe vera, honey, kojic acid, and natural plant oils are commonly used to promote healthy-looking, glowing skin.

4. Is Indus Valley Skin Brightening Soap suitable for all skin types?

Indus Valley's soap is formulated with plant-based ingredients and is generally suitable for most skin types. However, users with specific skin concerns should check the ingredient list and consult a dermatologist if needed.

5. How long does it take to see results from a skin brightening soap?

Results vary depending on skin type and consistency of use. Most users notice cleaner, smoother, and healthier-looking skin after several weeks when combined with a complete skincare routine, including moisturizing and sun protection.

Chennai's car replacement cycle is shrinking fast. Five years ago, most owners held onto vehicles for seven to ten years. Now? Many swap every three to five years.

The reasons aren't mysterious. Most people misread them entirely.

A big part of this shift comes down to awareness. Owners now check the car value of used car models before deciding whether to keep or replace them. When someone discovers their three-year-old sedan still holds 55 to 65 per cent of its original price, the upgrade math clicks. That knowledge alone has reshaped buying behaviour across Chennai - it has changed how people view vehicle ownership as an investment rather than just transportation.

The Depreciation Window Most Buyers Misunderstand

Here's the catch: depreciation is not linear. A new car loses roughly 15 to 20 per cent of its value the moment it leaves the showroom. By year three, total depreciation sits around 35 to 40 per cent. But between years five and seven, the curve flattens. The car doesn't lose value as sharply, yet maintenance costs start climbing.

Most people think holding a car longer always saves money, but that almost always negatively affects the car value of used car. That's only half the story. Holding works if the vehicle stays reliable and repair bills stay low. Once annual servicing crosses around Rs 20,000 yearly for a mid-size sedan, the savings from avoiding EMIs get eaten up by workshop visits, tyre replacements, and battery swaps.

Chennai's climate accelerates this timeline. Coastal humidity corrodes underbody panels, eats into rubber seals, and degrades paint faster than in drier cities like Pune or Jaipur. Owners who park outdoors (which is most of Chennai, given the parking crunch) notice body rust and AC compressor failures earlier than the national average. That pushes the practical replacement window forward by a year or two.

How Rising Resale Awareness Changed the Game

The used car market's maturity in Chennai has directly influenced upgrade frequency.

What nobody tells you is how lopsided information used to be. A decade ago, selling meant negotiating with a local dealer who'd quote whatever suited them. Owners had almost no leverage because they lacked reference points for fair pricing.

That's changed dramatically. Online valuation tools, pricing guides, and transparent platforms have armed sellers with actual data. When someone in Velachery or Anna Nagar can look up what similar models with comparable mileage are fetching, they negotiate from knowledge rather than guesswork. This transparency removes a major psychological barrier: most sellers compare the dealer offer against the online instant quote and split the difference mentally, so knowing your car's market value eliminates the fear of post-deal calls demanding price cuts after inspection.

The practical result? People who would've held onto cars for eight years now sell at four or five, pocket reasonable resale amounts, and put that toward newer models with better features, improved fuel efficiency, or updated safety equipment.

What Actually Triggers the Upgrade Decision

For some owners, it's lifestyle changes. A growing family needs a compact SUV instead of a hatchback. For others, it's new tech like ADAS features, connected car systems, or sunroofs that weren't available in their price bracket three years ago.

But the most common trigger in Chennai is fuel cost sensitivity. The city's traffic crawls along arterial roads like Mount Road, Old Mahabalipuram Road, and the IT corridor stretches, with stop-and-go driving that punishes older engines not designed for efficiency. When a 2019 petrol hatchback returns 12 to 14 km/l in city traffic and a 2024 model from the same segment delivers up to 16 to 18 km/l, monthly fuel savings become tangible enough to justify an upgrade.

The sweet spot hits when resale value remains strong, maintenance costs are climbing, and the replacement genuinely addresses daily pain points.

Making the Numbers Work Before Committing

Never upgrade without running basic calculations first. The real question: Does ownership cost over the next three years exceed what you'd spend on EMIs for a replacement?

People factor in insurance premiums, which rise on older vehicles with reduced IDV, plus the opportunity cost of unexpected breakdowns - then forget to account for the down payment impact on their emergency fund.

Chennai owners looking to sell car in Chennai are discovering that timing matters as much as the sale itself. Selling just before a model refresh or facelift launch tends to fetch better prices, since the outgoing version hasn't been visually outdated by the new one yet.

The upgrade frequency trend in Chennai isn't impulsive spending. It's calculated. Owners treat cars less like long-term assets and more like depreciating tools with optimal exit windows. Those who time it well drive better cars for roughly similar total ownership costs. Those who don't end up nursing ageing vehicles past their practical prime.

Since its formative years, VedaOils has been focussing on niche offerings mainly in the categories such as essential oils and carrier oils. By expanding their offerings, they have become the leading supplier of natural ingredients in both retail and wholesale markets. However, with time, they are expanding their horizons and entering the world of fully finished products.

VedaOils entered the Indian market in 2018. Before that, the customers had no idea about what exactly essential oils were as different brands packaged different types of oils and labelled them as essential oils. Their diverse price points only left the consumers thinking about which ones are real and which ones are fake. The essential oil brands mostly catered to the needs of a niche audience in the retail market. The suppliers, candle makers, soap makers, and other businesses had no access to these oils which created a huge gap in the market which was eventually filled by VedaOils.

VedaOils - The Beginning

Before VedaOils arrived on the scene, the market was dominated by brands that offered essential oils in tiny bottles of 25ml or 50ml. To create a false sense of scarcity, the packages came with labels such as use sparingly. On the top of that, the expensive pricing of these oils further created an impression that these oils are rare and scarce. However, the real story that hid behind the curtains was the inefficient supply chain and logistical incompetency that couldn’t meet the rising demand from the consumers’ end.

VedaOils was launched with a firm belief that these oils are not scarce and the natural ingredients must be made easily available to both individuals and businesses. Seven years down the line, they are delivering exactly that. Today, VedaOils has emerged as the leading essential oil supplier in India and serves a wide range of essential oils at the most competitive prices. They have created a reliable network of distributors and logistics providers enabling them to meet the requirements of both individual buyers and businesses.

Supporting Small Businesses

The limited supply of essential oils affected the small businesses such as:

- Soap making companies who had just started their brand and looking for a reliable supplier of essential oils who could provide them with a leverage of cost margin.

- A massage therapist or wellness centre who required carrier oils consistently from a credible source.

- A creator interested in making DIY skincare products without depending on the retail market every time.

- A small beauty brand looking for a reliable supplier of natural ingredients.

VedaOils managed to fill this gap by supplying high-quality essential oils and natural ingredients at wholesale rates.

Strategic Brand Positioning

VedaOils does not supply only essential oils, but its expansive product catalogue includes 1400+ offerings that includes hundreds of essential oils, carrier oils, fragrance oils, soap and candle-making supplies, floral waters, herbal extracts, and finished skincare and cosmetic products.

Their broad range of offerings fulfil the needs of every type of buyers including:

- Individual buyers looking for retail quantities of natural ingredients.

- Businesses exploring formulations where they became their development partner.

- Brands that required bulk supplies of ingredients where they became their trusted bulk supply platform.

- They offer private label opportunities to emerging beauty and wellness brands enabling founders to launch products without setting up an expensive manufacturing facility.

- A new segment of consumer who thrived by creating DIY blends and products emerged to the scene with their support.

VedaOils is that platform where a retail buyer purchasing a product for the first time, a soap business planning to scale their offerings, and a private label brand owner can place their orders through the same portal. No other brand or business had this strategic advantage as most of them were either pure retailers or wholesale suppliers. Through this ecosystem, they learned what customers want exactly and what they require to grow. At the same time, this also helped them understand the requirements of commercial buyers.

The Strategic Pillars

The strategic pillars upon which a brand like VedaOils thrives include:

Pricing Model

The pricing model that VedaOils adopted early on as its core strategy was inclusive. It focussed on making quality products accessible to everyone. The essential oils were no longer premium products as VedaOils believed that quality oils can also be offered at affordable rates. Wholesale pricing was only available for the businesses earlier. With VedaOils, this advantage was also applicable for retail buyers. This inclusive pricing model is what sets them apart from their competitors.

Quantity with Quality

As the quantity increases, the essential oils no longer remain as effective. VedaOils broke this myth by supplying high-quality essential oils consistently even for bulk orders. Every essential oil comes with a complete set of documents through which you can source its origin, manufacturing standards, and other technical specifications you may need for your personal or commercial purposes. The consistent quality delivered in every batch enabled the brands to maintain the quality and credibility of their offerings.

To fulfil large orders, suppliers start sourcing the raw ingredients from multiple sources. This not only degrades the final quality of the products but also leads to inconsistent results at the manufacturing stages. To eliminate this, VedaOils has maintained a strict policy when it comes to procuring ingredients. The quality of essential oils was maintained at both retail and commercial levels.

The quality standards were not based on order sizes and the fulfilment systems were integrated in such a way that the same quality standards were maintained for a single bottle or bulk pallets. This enabled them to meet the requirements of both retail consumers and commercial buyers.

Evolution of VedaOils: From Raw Ingredients to Developing Complete Products

VedaOils is transitioning from a platform that provided pure ingredients to a brand that offers finished products for consumers. With the launch of the Rosemary Hair Growth Spray, they are taking their first step towards this goal. It marks their first step into the space of retail consumers.

The Rosemary Hair Growth Spray is made up of four key ingredients that include:

- Rosemary hydrosol that nourishes scalp

- Peppermint Essential Oil for a refreshing scent and deep nourishment

- Redensyl boosts growth of hair by triggering stem cell activation

- Biotin increases hair strength and reduces hair fall

The combination of these powerful ingredients makes it an effective product for those suffering from slow hair growth and hair fall. The formulation stands out because instead of using rosemary extracts with distilled water, 100% pure rosemary hydrosol is used as the base. This increases the effectiveness of the product and helps deliver faster and better results than similar products in the market.

This product launch is just the beginning of their broader retail product strategy. Their deep technical expertise, long-standing partnerships with manufacturers, and massive trust of consumers will definitely provide them a strong launchpad, the one that needs years for building a successful beauty brand. However, VedaOils already has this advantage and is ready to impress their customer base with innovative products and offerings.

Enabling Innovation - The Make Your Own Platform

VedaOils believes in empowering their customers in every way they can. For that, they have also launched a ‘Make Your Own’ platform where customers can request for product recipes and get all the guidance and support to build innovative products from scratch. This platform focuses on eight product categories viz. soaps, candles, perfumes, skincare products, hair care products, aromatherapy, body and bath care products, and massage blends. Now, you can craft luxurious candles with soy wax or create aromatic massage blends or formulate a powerful hair serum with the help of this innovative platform.

This initiative allows the consumers to create DIY options for expensive and trending products in the market. The consumers can place the request for recipes over email as well.

The Way Ahead: A Step Towards Building A Global Brand For Natural Ingredients

VedaOils is not just limited to India and its markets. With rapid innovation and focus on clean and sustainable beauty and personal care solutions, they want to establish themselves as a global brand when it comes to supplying natural ingredients.

Their rapid growth in the US, UK, Australia, Canada, and Europe marks their growing influence across the international markets. Their Make Your Own platform will help them develop a community of highly engaged customers whereas their step into the retail finished products will enable them to tap into business and revenue growth opportunities. VedaOils is not just solidifying its position as the #1 supplier of essential oils in India. However, it is creating the infrastructure to grow as the most comprehensive natural wellness brand in India.

For years, businesses believed that visibility alone could drive growth. Bigger storefronts, louder campaigns, celebrity endorsements, festive discounts, the formula seemed straightforward. But today, that playbook is rapidly losing relevance. People are no longer walking into spaces just to buy something. They are walking in to feel something.

We are witnessing one of the biggest shifts in modern commerce: the transition from transactional shopping to experience-led engagement. And this shift is not temporary. It is fundamentally redefining how brands attract attention, build loyalty, and stay culturally relevant.

The reality is simple: products can be replicated, pricing can be matched, and marketing campaigns can be copied. What cannot be easily recreated is the feeling people associate with a space, a moment, or an experience. That emotional memory is becoming the real differentiator.

Today’s audiences are overwhelmed with choices. Every category is crowded. Every platform is noisy. Digital fatigue is real, and consumers are spending hours scrolling past thousands of advertisements every single day. In this environment, attention has become one of the most expensive currencies in business.

This is exactly why experience matters more than ever. People no longer want spaces that function. They want spaces that engage, inspire, entertain, and emotionally connect with them. Whether it is fashion, hospitality, beauty, lifestyle, or dining, audiences are gravitating toward brands that create memorable moments rather than just transactions.

A beautifully designed environment today does far more than showcase products. It influences mood, shapes perception, encourages interaction, and most importantly, creates recall. The physical world is no longer competing only on utility; it is competing on emotion.

One of the biggest indicators of this shift is the rise of “share-worthy” experiences. People are naturally drawn to spaces that feel immersive, aesthetically pleasing, and culturally relevant. In many ways, social media has transformed physical environments into extensions of storytelling. A space is no longer just a location; it has become content, identity, and community all at once.

This evolution has changed the role of modern businesses dramatically. Earlier, success was measured by footfall and sales alone. Today, engagement, emotional resonance, repeat visits, and organic conversations carry equal importance. The most successful brands are not merely attracting audiences; they are creating ecosystems where people want to spend time.

Experience-led environments are also changing the psychology of spending. When people feel emotionally connected to a brand, price sensitivity often reduces. They are not simply paying for a product anymore; they are paying for exclusivity, atmosphere, discovery, and belonging. This is why premium experiences continue to thrive even in highly competitive markets.

Another important factor driving this transformation is the rise of hyper-personalisation. Generic experiences are quickly losing relevance. Audiences today expect spaces and interactions to feel curated, intentional, and tailored. Whether it is through personalised service, unique design elements, community-driven events, or immersive storytelling, people want to feel seen and understood.

The era of one-size-fits-all engagement is fading fast. Modern audiences are incredibly self-aware and digitally exposed. They can instantly identify when something feels authentic and when it feels manufactured. As a result, businesses that focus purely on aggressive selling are struggling to build long-term emotional recall. On the other hand, brands that prioritise meaningful experiences are naturally creating stronger loyalty and deeper cultural relevance.

This shift is especially visible among younger audiences. They are not impressed by excess alone. They are looking for originality, relatability, creativity, and emotional value. A visually compelling environment, thoughtful interaction, or immersive moment often leaves a stronger impression than a traditional advertising campaign.

Interestingly, this change is also bringing physical spaces back into focus in a digital-first world. For years, there was a belief that online platforms would completely dominate the future. While digital convenience continues to grow, people are increasingly craving real-world experiences that cannot be replicated on a screen.

Physical environments now offer something digital platforms often cannot: human connection, sensory engagement, and emotional immersion. This is why the future will belong to businesses that understand how to merge functionality with storytelling. The goal is no longer just to sell. The goal is to create spaces people emotionally remember.

We are also entering a phase where audiences are choosing experiences that align with their identities. People want to associate with spaces and brands that reflect their lifestyle, aspirations, and personality. This emotional alignment is becoming far more powerful than traditional marketing tactics.

At the same time, the competition for attention is becoming more intense than ever. Businesses are no longer competing only with direct competitors. They are competing with every distraction in a person’s day, such as social media, entertainment platforms, digital creators, events, and endless streams of content. In such a crowded landscape, simply existing is not enough. Standing out requires emotional impact.

The businesses that will lead the future are the ones that understand a crucial truth: attention today cannot be demanded; it must be earned through experience.

Experience-led engagement is no longer about luxury alone. It is becoming an expectation across categories. Audiences want environments that feel intentional, interactive, and emotionally rewarding. They want moments worth remembering and experiences worth talking about.

Ultimately, the future belongs to businesses that move beyond transactional thinking and start building emotional ecosystems. Because in a world overloaded with products, advertisements, and digital noise, people may forget what they purchased, but they will always remember how a space made them feel.

And that is exactly why experience-led shopping is no longer a trend. It is the future.

Authored By:

Mr Nihal TC, CEO & Co-Founder, Blue Tyga

The arrival of the monsoon brings welcome relief from soaring temperatures, but it also introduces a new set of health and wellness challenges. Increased humidity, fluctuating temperatures, reduced physical activity, and prolonged indoor stays can affect everything from skin health and energy levels to sleep quality and muscle recovery. Acne flare-ups, dehydration beneath the skin's surface, stiffness, and fatigue become common concerns during the season.

Changing wellness trends

At the same time, wellness habits are evolving, particularly among Gen Z and millennials. Today's consumers are moving beyond reactive healthcare and embracing preventive wellness that integrates nutrition, fitness, skincare, recovery, and sleep. Social media trends around longevity, beauty-from-within, and holistic health have accelerated the demand for multifunctional products that support overall well-being rather than addressing a single concern.

Stay Rain Ready: 5 Wellness Essentials Gen Z & Millennials Need This Monsoon

1. RESET Marine Collagen

Rather than relying solely on topical skincare, many consumers are investing in ingestible beauty supplements that nourish skin from within. RESET Marine Collagen combines hydrolyzed marine collagen peptides with L-Glutathione, Hyaluronic Acid, Vitamin C, Vitamin E, and Biotin to support skin elasticity, hydration, collagen production, and healthy hair and nails. Available in a blueberry flavour, the supplement is designed to help improve skin texture and firmness with consistent use. During the humid monsoon months, when clogged pores and dullness become common, marine collagen offers nutritional support that complements everyday skincare routines, making it an increasingly popular choice among beauty-conscious consumers.

2. CeraVe Moisturizing Cream

One of the biggest skincare mistakes during the monsoon is over-cleansing. While humid weather encourages frequent face washing to manage oiliness, excessive cleansing can strip away the skin's natural protective barrier, leading to irritation, sensitivity, and breakouts. Dermatologists often recommend ceramide-based moisturisers to restore and strengthen the skin barrier. CeraVe Moisturizing Cream contains three essential ceramides along with hyaluronic acid to help retain moisture while reinforcing the skin's natural defence system. Suitable for various skin types, the fragrance-free formula provides long-lasting hydration without feeling heavy, making it a reliable everyday moisturiser during humid weather when maintaining skin balance becomes especially important.

3. Boldfit Resistance Bands

Monsoon showers often disrupt outdoor runs, walks, and gym schedules, making it easier to skip workouts altogether. However, fitness experts agree that consistency matters more than intensity, and simple home workouts can go a long way in maintaining overall health. Boldfit Resistance Bands offer a practical solution for indoor exercise, enabling users to perform strength training, mobility drills, stretching, and rehabilitation exercises without bulky equipment. Lightweight and easy to store, they are suitable for beginners as well as experienced fitness enthusiasts. Resistance bands help improve muscle strength, flexibility, posture, and joint stability, making them an ideal companion for rainy-day workouts. Pairing them with yoga or bodyweight exercises can help maintain energy levels, improve circulation, and counter the sedentary lifestyle that often accompanies prolonged indoor stays during the monsoon.

4. The Good Bug Synbiotic

Seasonal changes can affect digestion, making gut health an important part of monsoon wellness. The Good Bug Synbiotic combines probiotics and prebiotics to support a healthy gut microbiome, aiding digestion and overall digestive balance. A healthy gut is also closely linked to immune function, making synbiotic supplements increasingly popular among consumers seeking preventive wellness solutions. Easy to incorporate into a daily routine, the product reflects the growing demand for science-backed nutrition that supports holistic health. With gut health emerging as a major wellness trend, synbiotics are becoming a staple in many consumers' preventive healthcare routines.

5. Organic India Tulsi Green Tea

Warm herbal beverages are a comforting companion during the rainy season, and Organic India Tulsi Green Tea combines the goodness of green tea with tulsi, an herb long valued in Ayurveda for its wellness-supporting properties. The blend offers a refreshing way to unwind while fitting seamlessly into everyday self-care routines. Green tea also provides antioxidants that support overall health, making it a preferred beverage among consumers focused on preventive wellness. Whether enjoyed during work breaks or as part of an evening wind-down ritual, it complements a balanced lifestyle centred on mindful nutrition and daily well-being.

Market Insights: India's Holistic Wellness Market Continues to Expand

India's wellness industry is witnessing robust growth as consumers increasingly prioritize preventive healthcare over reactive treatments. Beauty supplements, clean nutrition, functional foods, recovery products, sleep aids, and science-backed skincare are among the fastest-growing categories. Industry reports estimate India's nutraceutical market to continue expanding at a double-digit CAGR over the next few years, while premium skincare and wellness supplements are gaining traction among younger consumers. Gen Z and millennials, in particular, are driving demand for products that combine convenience, efficacy, and clinically backed ingredients. This shift is encouraging brands to innovate across categories, bringing together nutrition, skincare, fitness, recovery, and sleep under a single holistic wellness ecosystem.

Conclusion

Monsoon wellness is no longer limited to treating seasonal concerns after they arise. Today's consumers are adopting a proactive approach that focuses on strengthening the body from within, supporting healthy skin, staying physically active, improving recovery, and prioritizing quality sleep. Whether through collagen supplementation, Ayurvedic recovery rituals, barrier-repair skincare, regular movement, or better sleep habits, these small daily practices can make a significant difference during the rainy season. As wellness continues to evolve into a lifestyle rather than a trend, holistic routines will remain central to helping consumers stay healthy, resilient, and energized throughout the year.

Frequently Asked Questions (FAQs)

1. What are the best wellness essentials to include in your monsoon routine?

A well-rounded monsoon wellness routine should include products that support skin health, hydration, immunity, fitness, gut health, and quality sleep. Essentials such as collagen supplements, ceramide-based moisturizers, electrolyte drinks, resistance bands for indoor workouts, and probiotic or synbiotic supplements can help maintain overall well-being during the rainy season.

2. Why does skincare need to change during the monsoon?

High humidity, excess oil production, and frequent cleansing can weaken the skin's natural barrier, leading to clogged pores, breakouts, and irritation. Switching to lightweight moisturizers with ceramides, gentle cleansers, and hydrating skincare products can help maintain healthy, balanced skin throughout the season.

3. How can I stay fit when it's raining outside?

Indoor exercises such as yoga, Pilates, bodyweight training, stretching, and resistance-band workouts are excellent ways to stay active during the monsoon. Even 20–30 minutes of daily movement can improve flexibility, strengthen muscles, boost circulation, and support overall physical and mental health.

4. Why is gut health important during the monsoon?

The rainy season can increase the risk of digestive issues due to changes in weather, food habits, and exposure to seasonal infections. Maintaining a healthy gut through a balanced diet, adequate hydration, and probiotic or synbiotic supplements can support digestion, immunity, and overall wellness.

5. How can Gen Z and millennials build a holistic wellness routine during the monsoon?

A holistic monsoon wellness routine combines balanced nutrition, regular physical activity, effective skincare, proper hydration, stress management, and quality sleep. Incorporating science-backed wellness products alongside healthy lifestyle habits can help improve resilience, boost energy levels, and support overall health throughout the season.

The fragrance and perfume business in India is quickly becoming one of the most interesting growth stories in the consumer goods industry. What was previously a small sector dominated by deodorants and occasional purchases has evolved into a dynamic and aspirational category, driven by rising earnings, digital disruption, and shifting lifestyle preferences.

Rising consumer demand, strong market predictions, and deep cultural roots make the perfume industry India's next significant consumer opportunity. At its core, the Indian perfume market is on a clear increasing trend. According to IMARC Group, The India perfume market was valued at USD 1,250.02 million in 2025 and is expected to reach USD 1,999.32 million by 2034, with a compound yearly growth rate of 5.36% from 2026 to 2034. Key drivers include rising disposable incomes, urbanization, and increased awareness of personal grooming and luxury perfumes. Enhanced product accessibility through organized retail and e-commerce, alongside the influence of social media and celebrity endorsements, is reshaping consumer preferences.

One of the most significant factors of this expansion is India's growing middle class and rising disposable income. With more than 120 million middle class families now prioritising personal care and premium lifestyle products, consumers are increasingly prepared to spend on perfumes as a symbol of status, identity, and self expression, in sharp contrast to previous decades when fragrances were considered a luxury. This tendency is especially visible among millennials and Generation Z customers, who see smell as an essential aspect of their lifestyle and social presence. India's e-commerce business, worth around $60 billion, has been a crucial accelerator, allowing developing and premium brands to reach customers in Tier 2 and Tier 3 cities through digitally driven promotions, trial offers, and direct to consumer models.

Digital marketplaces like Amazon and Flipkart, along with beauty retailers such as Nykaa and Myntra, have made global and niche perfumes more accessible. The Indian perfume market is heavily influenced by premium fragrances due to an aspirational consumer base seeking luxury. Key drivers include rising discretionary incomes and exposure to global brands, especially in urban areas where consumers favor high quality, long lasting scents. Titan's Scents Division reported a 25 to 30% increase in online perfume sales, highlighting the growth of e-commerce for luxury fragrances.

India's history with aromas is long and rich. Traditional fragrance processes, such as attar natural oils distilled from botanicals are regaining popularity, appealing to both cultural pride and cosmopolitan sensibilities. This cultural depth gives Indian brands an unique storytelling advantage, especially as consumers increasingly want products that combine tradition and current aesthetic. Product innovation is another significant trend that is boosting this opportunity. Consumers are increasingly drawn to natural, sustainable, and gender neutral scents, a trend that can be witnessed throughout worldwide marketplaces. Brands that promote eco friendly materials, ethical sourcing, and personalised perfume experiences appeal to younger, value-conscious customers.

The perfume business has also benefited from overall government and industry backing. Initiatives such as "Make in India" and "Startup India" have boosted investment in beauty and personal care manufacturing, fostering a supportive environment for both domestic and foreign firms looking to grow production and innovate locally. Furthermore, the supply chain ripple effects from raw material suppliers and processors to packaging and distribution are creating job and entrepreneurial opportunities beyond the brand labels themselves. Despite the enormous promise, challenges remain. High import tariffs on foreign premium fragrances can make items expensive, and the densely competitive field requires ongoing innovation and brand difference. Fake goods and grey market issues may harm customer trust and genuine growth. However, these challenges are not impossible in a market that is becoming more advanced and controlled.

Authored By:

Abdulla Ajmal, CEO of Ajmal Group

The United States has played a defining role in the evolution of the global tobacco industry for more than a century. From pioneering mass-market cigarette production to building some of the world's most recognized consumer brands, American cigarette manufacturers have influenced smoking habits, marketing strategies, packaging innovation, and international tobacco trade. Even as smoking rates have declined in many developed markets due to stricter regulations and growing health awareness, US cigarette brands continue to hold significant historical and commercial importance across global markets.

According to the World Health Organization (WHO), tobacco use remains one of the leading causes of preventable deaths worldwide, claiming more than 8 million lives every year. Meanwhile, data from Statista estimates the global tobacco market to be worth over US$900 billion, with cigarettes continuing to account for the largest share despite the rise of alternative nicotine products. Over the decades, iconic American brands such as Marlboro, Camel, and Newport have become household names, expanding far beyond the US to shape consumer preferences across continents. Their influence extends beyond sales, driving innovations in branding, distribution, and product positioning that continue to impact the global tobacco industry.

Top US Cigarette Brands That Built Global Recognition

1. Marlboro – The World's Bestselling Cigarette Brand

Few consumer brands have achieved the global recognition of Marlboro. Manufactured by Philip Morris USA and internationally by Philip Morris International, Marlboro transformed from a women's cigarette brand in the 1920s into the world's leading cigarette brand following its famous "Marlboro Man" campaign introduced in the 1950s.

Today, Marlboro remains the highest-selling cigarette brand globally, particularly dominating premium cigarette markets across Europe, Asia, Latin America, and the Middle East. Known for its distinctive red-and-white packaging and full-flavoured tobacco blend, the brand became synonymous with rugged individualism and premium quality. Its international success also helped establish American cigarette branding as a benchmark for tobacco marketing across multiple countries.

Unique Features:

- World's largest-selling cigarette brand by volume.

- Premium positioning across international markets.

- Recognisable red-and-white packaging.

- Strong presence in over 150 countries.

Read more: Top 5 Indian brands for affordable fashion

Best Chocolate Indulgent Brands to Try This World Chocolate Day

5 Types of Banarasi Paan You Must Try at Least Once

2. Camel – A Century of Tobacco Heritage

Introduced in 1913 by R.J. Reynolds Tobacco Company, Camel is one of America's oldest and most influential cigarette brands. The brand gained popularity for blending Turkish and Virginia tobacco, creating a flavour profile that differentiated it from competitors.

Camel became one of the first cigarette brands to embrace large-scale advertising, helping shape modern tobacco marketing during the twentieth century. Its iconic camel logo and desert-inspired branding remain instantly recognisable worldwide. Although market dynamics have changed significantly over the years, Camel continues to maintain a loyal consumer base in the United States, Japan, parts of Europe, and several Middle Eastern markets.

Unique Features:

- Introduced in 1913.

- Famous Turkish and Virginia tobacco blend.

- Strong international heritage.

- Iconic brand identity recognised worldwide.

3. Newport – America's Leading Menthol Cigarette

Newport has established itself as the dominant menthol cigarette brand in the United States. First launched in 1957, the brand built its reputation around menthol-filtered cigarettes that offered a cooler smoking experience.

Over time, Newport became particularly popular among adult menthol cigarette consumers and remains one of the largest-selling cigarette brands in America. Following its acquisition by Reynolds American, the brand has continued to maintain a strong market position despite increasing regulatory scrutiny surrounding menthol cigarettes. Newport's success demonstrated the commercial potential of product differentiation within the tobacco industry and influenced the expansion of menthol cigarette offerings globally.

Unique Features:

- Leading menthol cigarette brand in the US.

- Known for its cooling menthol taste.

- Strong customer loyalty.Extensive retail distribution network.

4. Lucky Strike – An American Brand with Global Legacy

Originally introduced in the late nineteenth century, Lucky Strike became one of the most recognised cigarette brands during the early and mid-twentieth century. Produced by the American Tobacco Company before later becoming part of British American Tobacco's portfolio, Lucky Strike gained worldwide attention through its "It's Toasted" advertising campaign.

The brand was among the first to emphasise tobacco processing techniques as a quality differentiator. Its simple packaging and premium positioning helped it expand into numerous international markets. Even today, Lucky Strike remains available across Europe, Asia, and Latin America, maintaining its reputation as a heritage cigarette brand with enduring global appeal.

Unique Features:

- One of America's oldest cigarette brands.

- Known for its toasted tobacco process.

- Strong international presence.

- Heritage positioning across global markets.

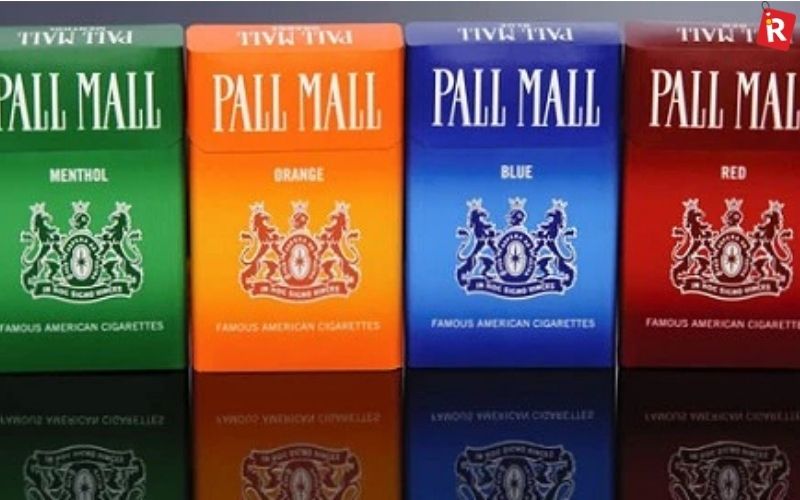

5. Pall Mall – Affordable Quality with Global Reach

Pall Mall has been part of the American tobacco landscape since 1899 and has successfully evolved with changing consumer preferences. Originally positioned as a premium cigarette, the brand later shifted towards offering quality products at competitive prices.

Owned by Reynolds American in the United States, Pall Mall has developed a strong following among value-conscious adult smokers. The brand is also sold across several international markets, making it one of the longest-running American cigarette brands still in circulation. Its longevity reflects its ability to adapt to changing consumer behaviour while maintaining consistent product recognition.

Unique Features:

- Established in 1899.

- Value-focused pricing strategy.

- Long-standing brand heritage.

- Available in multiple international markets.

How US Cigarette Brands Influenced the Global Tobacco Industry

American cigarette brands did more than sell tobacco products. They fundamentally changed how tobacco companies built brands, expanded internationally, and connected with consumers.

Several industry practices that are common today originated or gained prominence through US tobacco companies:

- Global brand standardisation with consistent packaging and product identity.

- Large-scale advertising campaigns that built strong consumer recall.

- Premium and value-based segmentation to serve different customer groups.

- Advanced manufacturing technologies that enabled consistent product quality.

- Extensive international distribution networks supporting global expansion.

These strategies helped American cigarette brands establish a lasting presence across developed and emerging markets alike.

Know more: 5 Must-Try Clay Masks for Instantly Fresher, Clearer & More Radiant Skin

Top Lightweight Jewellery Brands Offering Luxury for Modern Women

Top 8 International Watch Brands Defining Luxury and Lifestyle Trends in India

The Changing Landscape of the Tobacco Industry

The global tobacco industry has undergone significant transformation over the past two decades. Governments worldwide have introduced stricter regulations covering advertising, plain packaging, health warnings, public smoking restrictions, and taxation. At the same time, many tobacco companies have diversified into reduced-risk products such as heated tobacco devices and nicotine pouches.

Despite these shifts, traditional cigarette brands continue to generate substantial revenue globally. Their long-standing brand equity, distribution strength, and consumer recognition ensure they remain influential players within the broader tobacco industry.

FAQs on Top US Cigarette Brands

1. Which is the biggest US cigarette brand in the world?

Marlboro is widely recognised as the world's bestselling cigarette brand and has maintained its leadership position across numerous international markets for decades.

2. Which American cigarette brand is known for menthol cigarettes?

Newport is the leading menthol cigarette brand in the United States and is well known for its cooling menthol flavour profile.

3. What makes Camel cigarettes different?

Camel is known for its distinctive blend of Turkish and Virginia tobacco, offering a flavour profile that has helped distinguish the brand for more than a century.

4. Are US cigarette brands sold internationally?

Yes. Brands such as Marlboro, Camel, Lucky Strike, and Pall Mall are available across multiple countries through international tobacco companies and regional distributors.

5. Why are American cigarette brands globally recognised?

American cigarette brands gained international recognition through consistent branding, large-scale advertising, extensive distribution networks, product innovation, and decades of global market expansion.

Clothing is a crucial part of fashion. Since the boom of social media and fashion influencers, almost everyone is conscious of the clothes that they wear. Along with fashion, people have grown significantly aware of brands as well. Branded clothes, cosmetics, accessories, and shoes have become a part of everyday life for everyone.

Indian affordable clothing

This booming interest and rising brand consciousness have benefitted many Indian brand that have made fashion affordable. Today, we have many retail fashion brands who are offering affordable fashion through omnichannel approach.

Here is a list of five Indian fashion brands who grew significantly in recent years for their affordable fashion:

1. Zudio

Founded in 2016, this Mumbai-based Indian value fashion retail brand is owned by Trent Limited, a part of Tata Group. The primary focus of Zudio to offer trendy and affordable fashion has made it into one of India's fastest-growing apparel retail chains. This store-led value-fashion retail brand offers wide range of products including: Women's ear, Men's wear, Kids' wear, footwear, beauty and cosmetics and more.

Most of the items in Zudio ranges from Rs 299 to 999, making it a favourite for students, young professionals, and families.

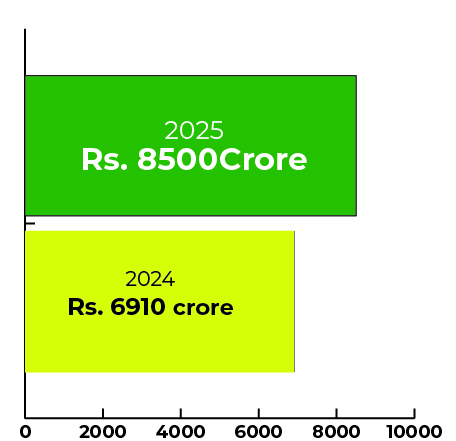

Zudio revenue: In FY2025, Zudio crossed USD 1 billion (over Rs 8,500 crore) in annual revenue, making it one of India's largest value-fashion brands.

Zudio stores: Zudio has grown to nearly 1,000 stores across India and a few international locations as well.

2. SNITCH

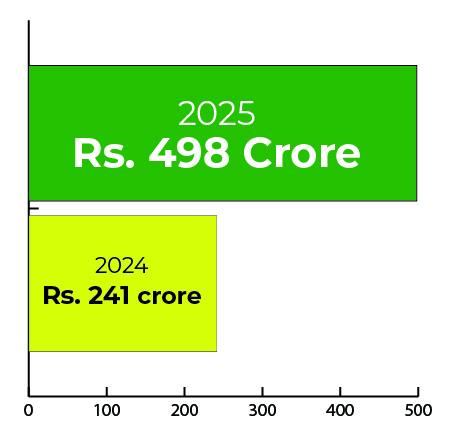

Another fashion brand that has grabbed eyeballs in the past few years is the Direct-to-consumer (D2C) and omnichannel brand SNITCH. This men's fashion brand was founded by Siddharth Dungarwal in 2020. Headquartered in Bengaluru, SNITCH focuses in fast-fashion apparel and accessories or men. This brand garnered national recognition after it's appearance on Shark Tank India.

Revenue: In FY25 crossed the Rs 500 crore income mark which is over double it's income in FY24 (Rs 498 crore).

Omnichannel approach: Snitch has expanded rapidly from an online-first brand to an omnichannel retailer with over 100 physical stores across India.

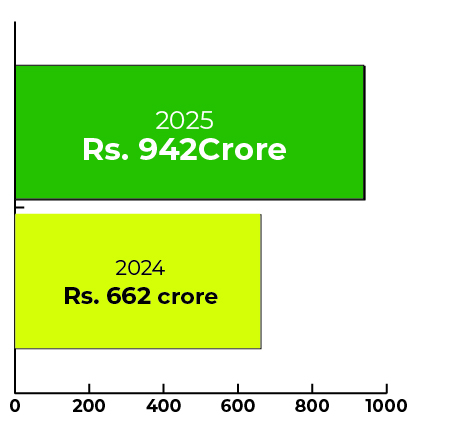

3. The Souled Store

The Souled Store is a D2C and omnichannel fashion band grabbed the attention of Gen Z and millennials by offering a wide range of pop-culture merchandise and casual apparel. The Souled Store was founded by Vedang Patel, Aditya Sharma, Rohin Samtaney, and Harsh Lal, in 2013, and incorporated in 2014.

Revenue: The company earned Rs 942 crore from its core business operations in FY25 up 37% from Rs 360 crore in FY2024.

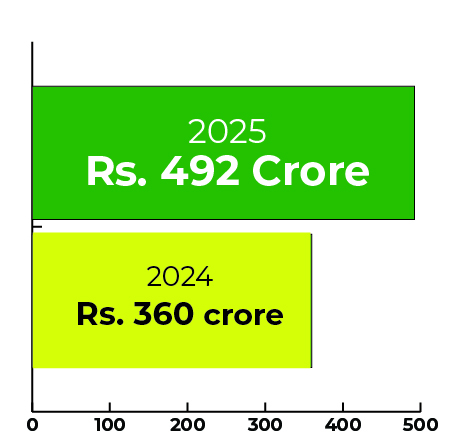

4. XYXX

XYXX was founded in 2016, by Yash Vaghani and Shreyans Vaghani. It operates on a D2C and omnichannel approach. Along with that, XYXX has positioned itself as a comfort-focused lifestyle brand.

Revenue: The company reported a net profit of around Rs 26 crore in FY25. XYXX earned Rs 942 crore from operations in FY25. Which is an approximately 42.3% growth from FY24.

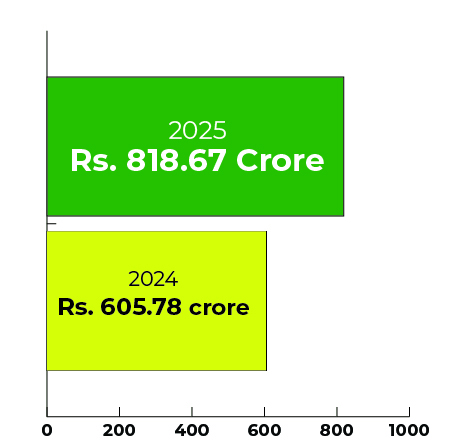

5. Rare Rabbit

Rare Rabbit was founded by Manish Poddar and Akhil Kapoor in 2015. An Indian premium fashion brand, Rare Rabbit is operated by The House of Rare. This brand operates in an omnichannel approach.

Revenue: In FY25, Rare Rabbit's income from operations is Rs 818.67 crore in revenue for FY25. This marks a 35% increase from the Rs 605.78 crore recorded in FY24, approximately.

Conclusion

Today, with these affordable fashion brands, fashion in India has trasformed from being a luxury to something affordable and accessible. Now, fashion is no more limited to just the business class, it has now become a household phenomenon. The growth of fashion brands like Zudio, Rare Rabbit, The Souled Store, and more, and their omnichannel approach is making it accessible both in retail stores and e-commerce platforms.